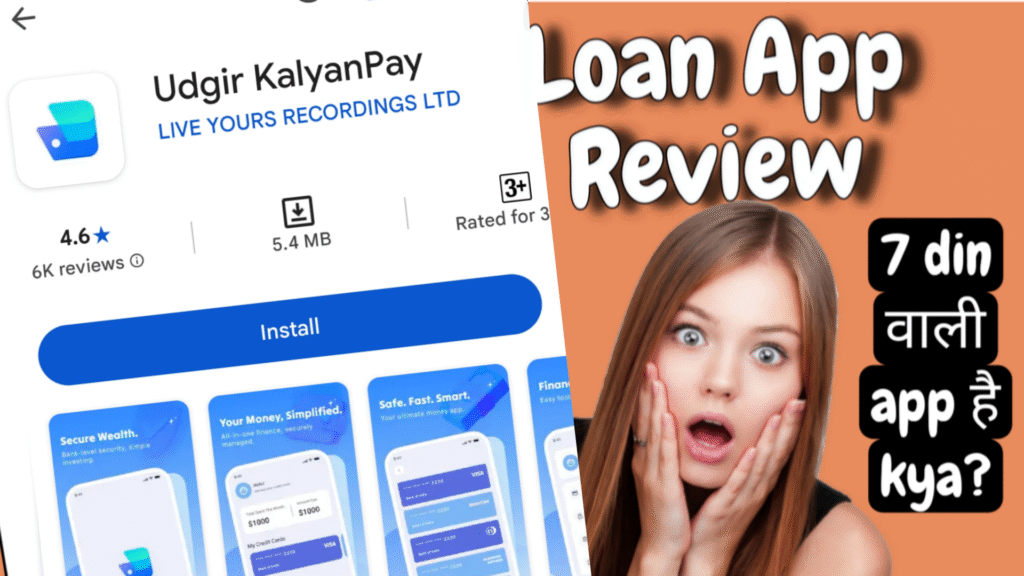

VeryCredit – Credit Assistant App Review: VeryCredit Loan Real or Fake? जाने

Aajkal instant loan apps bahut popular ho gaye hain India mein, especially jab urgent paise ki zarurat hoti hai. Ads mein dikhte hain low interest rate, quick approval, aur easy repayment. Lekin reality bilkul alag hoti hai. Aaj hum baat karenge VeryCredit – Credit Assistant app ki, jo Play Store pe available hai (package name: com.verycredit.getscore ya similar variants jaise VaniCredit related). Ye app basically 7-day loan provide karti hai, matlab sirf 5-7 din mein pura amount + heavy interest repay karna padta hai.

Important Warning: Is app ke description mein bahut achhi cheezein likhi hui hain jaise credit score check, budget management, safe data, etc. Lekin users ke critical reviews (especially 1-star) se pata chalta hai ki ye ek heavy charge wali trap app hai. Play Store pe filter karke 1-star reviews dekho – wahan real complaints milengi fraud, hidden charges, harassment, aur short repayment time ki.

VeryCredit App Kya Hai Aur Kaise Kaam Karti Hai?

Ye app claim karti hai ki ye credit assistant hai jo aapke credit status ko improve karne mein help karegi. Lekin asal mein ye instant personal loan deti hai small amounts mein (jaise 2000-10000 Rs). Ads mein lowest interest rate dikhaate hain, lekin apply karne pe approval ke baad sirf partial amount disburse hota hai, aur repayment amount double ya triple ho jata hai sirf 6-7 days mein.

Example se samjho:

- Agar aap 5000 Rs apply karte ho, to sirf 3000-3500 Rs milte hain.

- Repay karna padta hai 5000-6000+ Rs just 6 days mein.

- Interest effectively 50-100%+ ho jata hai short time ke liye – ye bahut heavy charges hain!

Play Store pe overall rating shayad 4.4 dikhta hai kuch positive reviews se, lekin negative reviews mein log bol rahe hain “totally fraud”, “fake app”, “don’t download”.

Play Store Critical Reviews – Real User Experiences (Desi Style)

Yahan kuch real 1-star reviews hain jo users ne February 2026 mein post kiye (jaise aapke shared screenshots se):

- Adarsh Ranjan (23/02/26): “Don’t download this app, totally fraud, and they force u to pay 2000 rupees to clear your data, otherwise they call your family by the data u shared, totally fraud… they don’t have any customer care services.”

Bhai log, ye serious hai – data misuse aur family ko call karna harassment ka sign hai! - Gopi Tadisetty (22/02/26): “Fake app 3000 loan amount transfer only 1800 repayment only 6 days collect the 3000 amount only interest 1200.”

Matlab: 3000 maange, sirf 1800 mile, 6 din mein 3000 + 1200 interest – total loot! - Mithun Sethi (23/02/26): “Not good only 6 days time if you apply 5000 you will get only 3100 but repay 5200 Don’t Apply.”

Clear trap – disbursed kam, repay zyada, time bahut kam. - Devendra Pandey (18/02/26): “Total fake app. On ads showing lowest interest rate… credited 2.4k only and showing repayment of 4k just after 5 days… uske bad jb inhone application fill krwai personal details… 23% diya fake app.”

Ads mein low interest, reality mein 23%+ hidden charges. - Laxmi Gupta (20/02/26): “They disbursed only 3700 but the repayment amount is 6700… that much they are taking… very worst thing and also they are giving only 6 days.”

Almost double amount maang rahe hain – ye bahut bura hai!

In reviews mein common complaints:

- Disbursed amount kam (half ya usse bhi kam)

- Repayment double/triple short time mein

- No proper customer care

- Data misuse aur family harassment

- Ads fake promises

Ye sab reviews bahut helpful votes pa rahe hain (jaise 3 se 55 tak), matlab real users agree kar rahe hain.

Kyun Inke Description Pe Bharosa Nahi Karna Chahiye?

App description mein likha hota hai “safe”, “reliable”, “credit insights”, “budget tracking”. Lekin ye sirf attract karne ke liye hai. Real mein ye 7-day loan trap hai jahan heavy interest lagta hai. Bahut saare similar apps jaise fake loan apps RBI registered nahi hote, foreign links hote hain, aur harassment karte hain.

Government bhi warn karta hai aise apps ke against – cybercrime.gov.in pe report karo agar fraud ho.

Pros Aur Cons (Honest View)

Pros (sirf thode):

- Quick apply process (lekin trap ke liye)

- Small loans available urgent need mein

Cons (bahut zyada):

- Heavy hidden charges aur interest

- Short repayment tenure (5-7 days)

- Partial disbursement

- Harassment calls/family threats

- No real customer support

- Data privacy risk

Overall: Avoid karo! Better hai RBI-approved apps ya banks se loan lo.

Agar Aapke Saath Fraud Hua Hai To Kya Karein? Complaint Kaise Karein

Agar aapne ye app use kiya aur fraud feel ho raha hai (jaise extra charges, harassment, data misuse), to turant action lo:

- Play Store pe report karo – App ko flag karo as inappropriate/fraudulent.

- Cyber Crime Portal pe complaint file karo:

- Jaao cybercrime.gov.in

- “Report Other Cyber Crime” select karo

- Details daalo: App name, amount, screenshots, calls/transactions proof

- Helpline: 1930 call karo (National Cyber Crime Helpline)

- Bank/NPCI se contact agar UPI/bank transfer hua – block karwao aur dispute raise karo.

- Police station mein FIR – Local cyber cell ya nearest PS mein jaake complaint do.

- Consumer Forum – Agar amount bada hai to online consumer complaint file kar sakte ho.

Yaad rakho: Kabhi bhi darr ke extra paise mat do blackmail pe. Report karo – government action leti hai aise apps pe.

FAQ – VeryCredit App Ke Baare Mein Common Questions

Q1: VeryCredit app real hai ya fake?

A: App Play Store pe hai, lekin users ke according fake practices – heavy charges, fraud disbursement. Critical reviews dekho, description pe mat jaao.

Q2: Interest rate kitna hai?

A: Ads mein low dikhaate hain, lekin reality mein 50-100%+ effective interest short 6-7 days mein. Hidden charges bahut.

Q3: Loan kitne din mein repay karna padta hai?

A: Sirf 5-7 days – bahut tight timeline, miss kiya to harassment shuru.

Q4: Customer care number hai?

A: Users bol rahe hain no proper support. App mein koi real helpline nahi milta.

Q5: Safe hai data share karna?

A: Nahi – reviews mein family calls aur data misuse ki complaints hain.

Q6: Better alternatives kaun se?

A: RBI-approved NBFC apps jaise MoneyTap, CASHe (lekin unke bhi reviews check karo), ya bank personal loan. Urgent need mein family/friends se better.

Q7: Main apply kar chuka hoon, ab kya?

A: Repay on time agar possible, lekin agar harassment ho to turant cyber complaint karo. Extra mat do.

Bhaiyon aur behno, aise apps se dur raho. Paisa urgent ho to soch samajh ke loan lo. Bahut saare log trap mein fas jaate hain aur phir pareshan hote hain. Share karo ye article agar kisi ko help ho.

(Word count: approx 1450+ – full details ke saath)

Stay safe, stay aware! 🚨